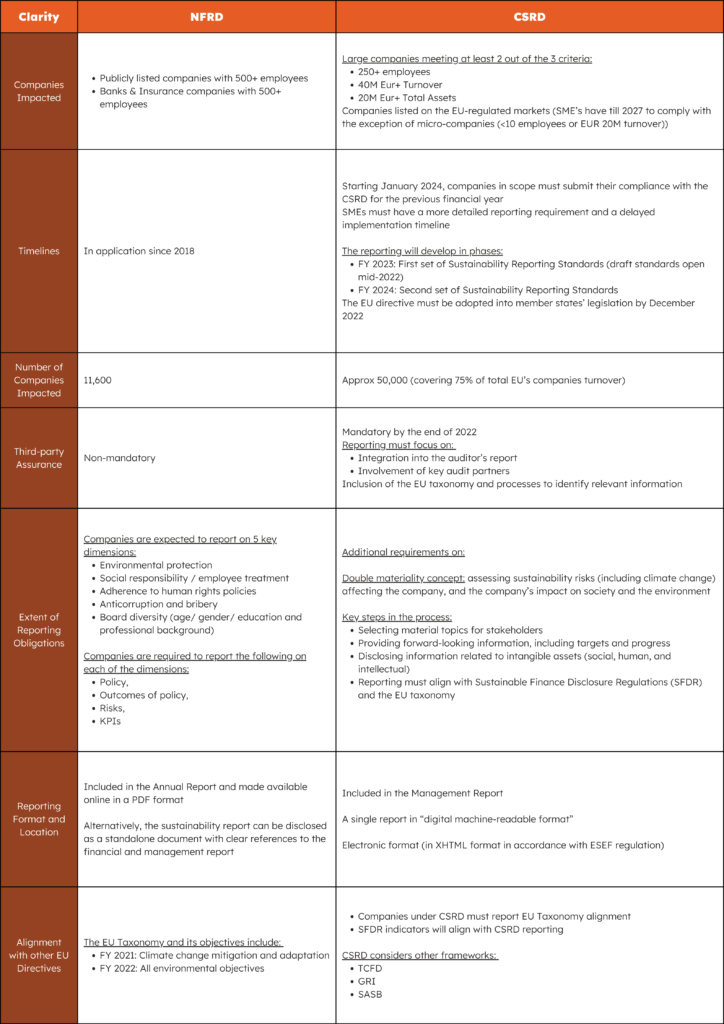

The CSRD is a significant advancement in sustainability reporting, building upon the foundation laid by the NFRD, which was adopted in 2014. The NFRD was a pioneering regulation aimed at increasing transparency and accountability by requiring large public-interest entities (PIEs) with over 500 employees to disclose non-financial information. This included data on environmental impact, social responsibility, treatment of employees, human rights, and anti-corruption measures.

While the NFRD represented a critical step forward, its limitations became evident over time. The scope was confined to a relatively small group of companies, and the reporting requirements lacked the detail and standardization necessary for comprehensive assessments and comparisons. Additionally, the NFRD did not mandate external assurance of the reported information, raising concerns about the accuracy and reliability of the data.

The CSRD addresses these shortcomings by significantly broadening the scope of reporting entities and introducing more detailed and standardized reporting requirements. It covers a much wider range of companies, including all large companies (with over 250 employees and/or €40 million in turnover and/or €20 million in total assets) and all listed companies (except listed micro-enterprises). These companies are required to disclose detailed information on various ESG topics, including climate change, biodiversity, human rights, and social responsibility, using a set of mandatory ESRS.

Furthermore, the CSRD mandates external assurance of sustainability information, ensuring the accuracy and reliability of reported data. It also introduces a “double materiality” perspective, requiring companies to report on both the impact of their activities on the environment and society, as well as the impact of sustainability matters on their financial performance. This comprehensive approach aims to provide stakeholders with a complete picture of a company’s sustainability performance and its potential financial implications.

Graph 1: NFRD vs. CRSD comparison

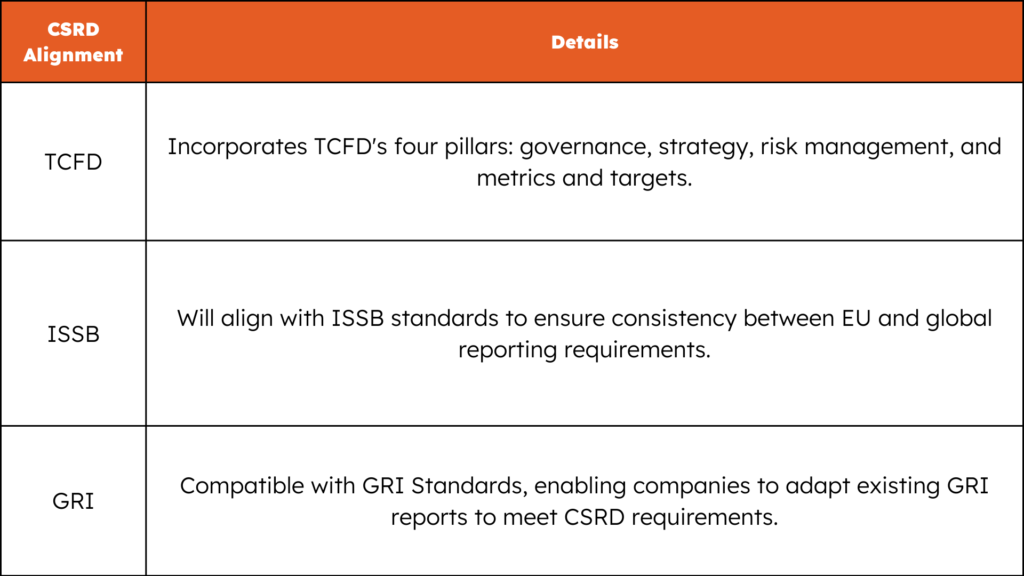

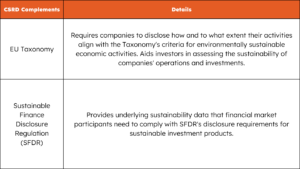

The CSRD interacts with the other frameworks in several ways:

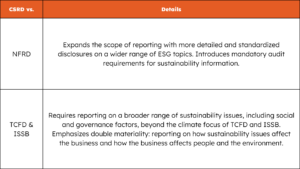

Expanding and Deepening Disclosure Requirements:

Supporting the EU’s Sustainable Finance Agenda:

The CSRD acts as a central pillar in the EU’s sustainable finance framework. It builds upon and aligns with existing frameworks like TCFD and GRI, while expanding and deepening disclosure requirements. By requiring comprehensive and standardized sustainability reporting, the CSRD aims to enhance transparency, comparability, and accountability, ultimately contributing to a more sustainable economy.

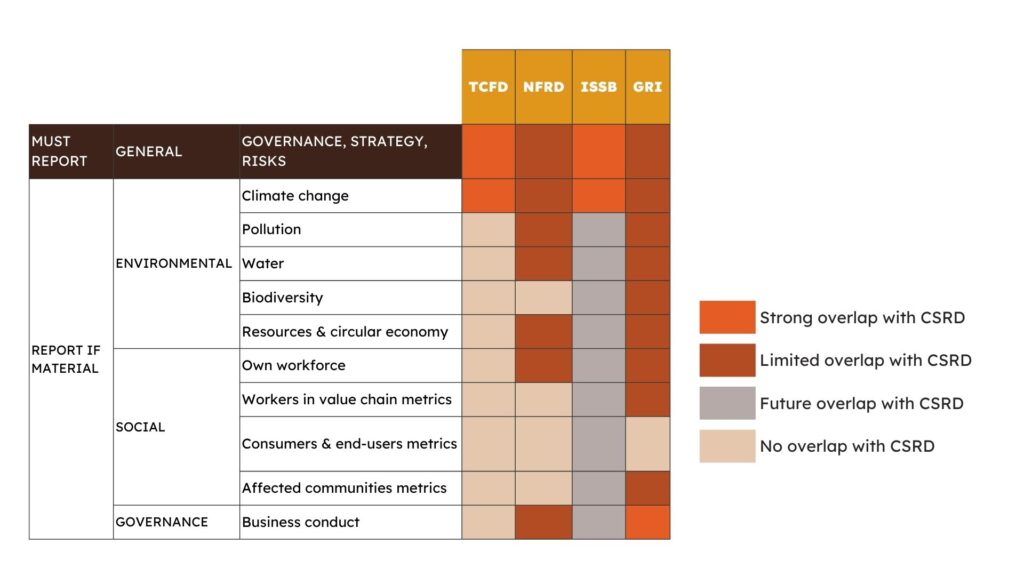

Graph 2: NFRD vs. CRSD comparison

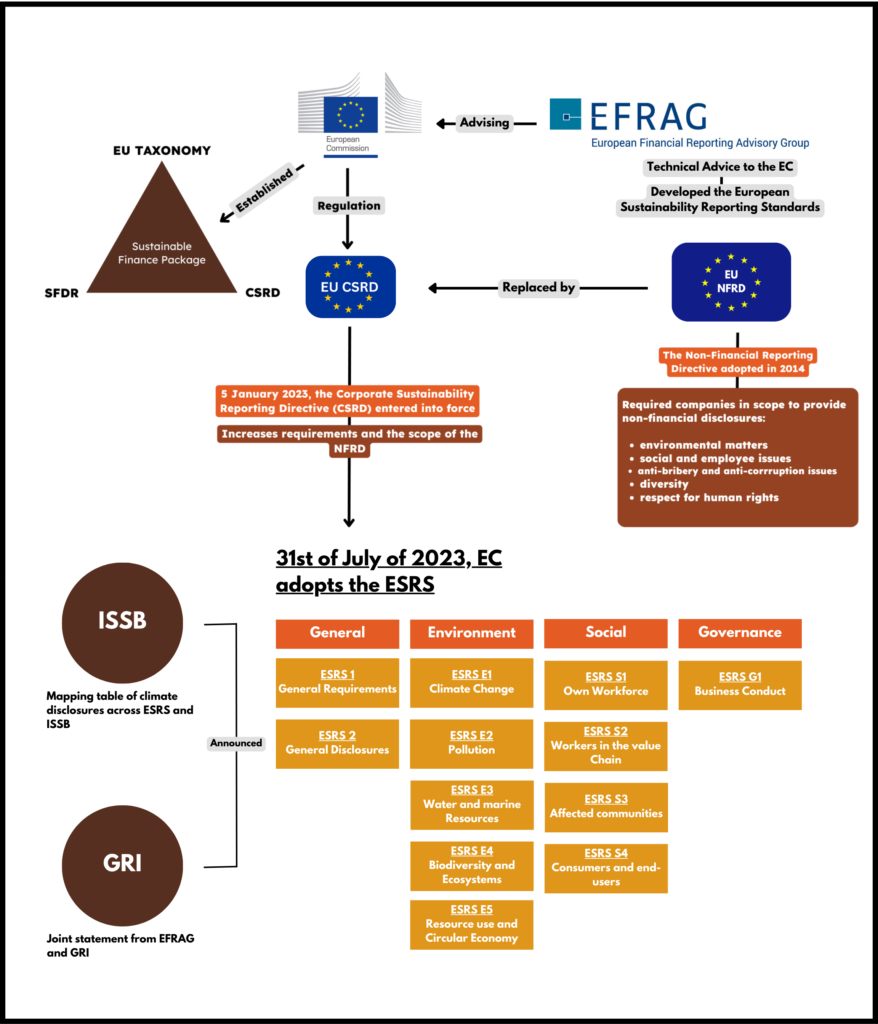

Graph 3: How it all fits together in EU

Eligibility Criteria for companies

Large EU public interest companies already reporting under the NFRD must continue to do so if they meet the following criteria:

Reporting due: Calendar year 2025, based on data from the financial year 2024

All large companies must report if they meet at least two of the following updated criteria:

Reporting due: Calendar year 2026, based on data from the financial year 2025

Phased-in reporting from 2025 to 2029 for large companies, based on specific criteria

All listed SMEs are required to report, unless they choose to opt out for two years.

SMEs meet a maximum of two of the following updated criteria:

Reporting due: Calendar year 2027 (or 2029 if opted out), based on data from the financial year 2026 (or 2028 if opted out)

Subject to a simplified set of ESRS standards

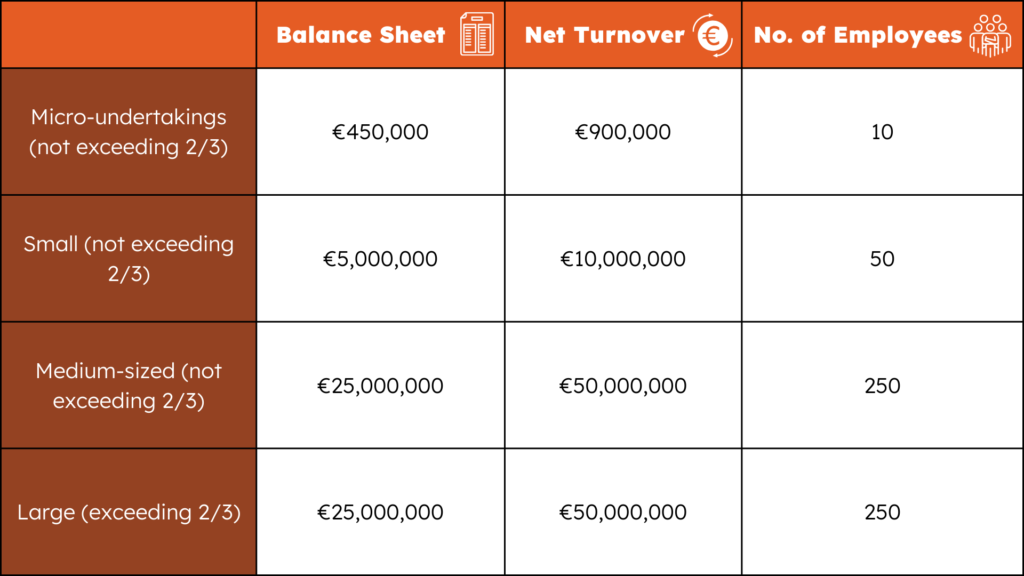

For smaller undertakings, the ESRS offers flexibility in financial thresholds. While Member States have the authority to set their own specific limits, these cannot exceed:

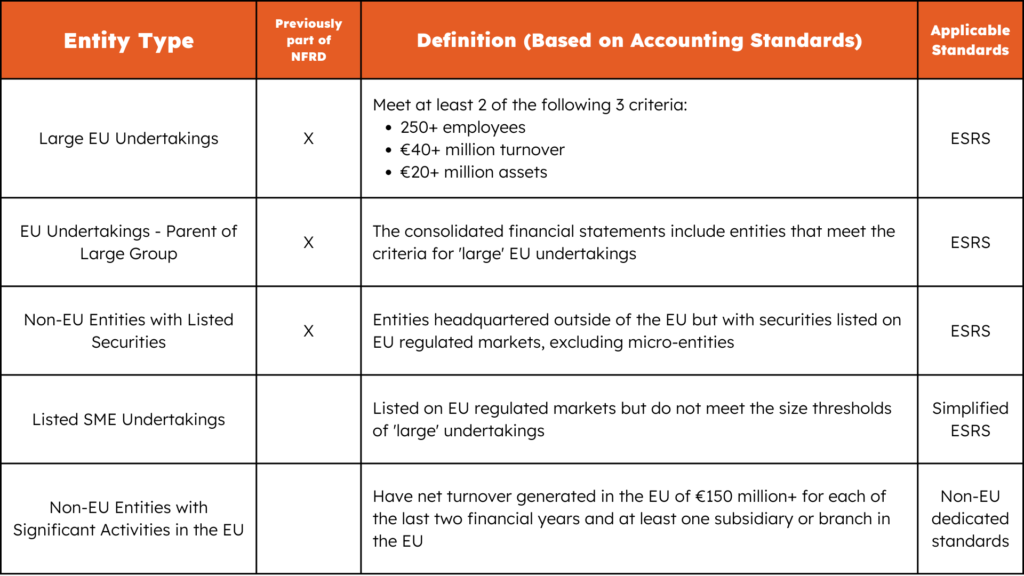

Graph 4: Summary of entities within the scope of CSRD

This overview provides a comprehensive understanding of the entities covered by the CSRD and their respective reporting timelines, considering the recent adjustments to the Accounting Directive’s size criteria.

Graph 5: Applicable standards for CSRD entities

The introduction sets the stage for understanding the significance and impact of the Double Materiality Assessment, highlighting its relevance under the CSRD and its extensive reach.

The Double Materiality Assessment is a core component of the Corporate Sustainability Reporting Directive (CSRD), set to significantly change corporate sustainability reporting. This guide aims to help companies understand and implement this comprehensive reporting framework, which will impact around 50,000 companies. The CSRD mandates that companies report on how various sustainability issues affect ESG topics and vice versa, reflecting a comprehensive view of their environmental and social responsibilities.

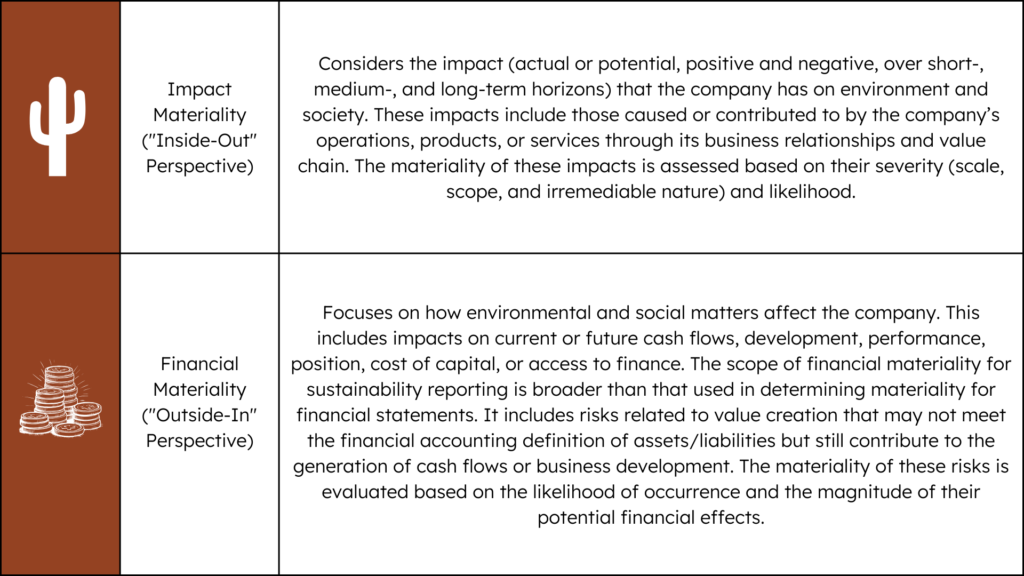

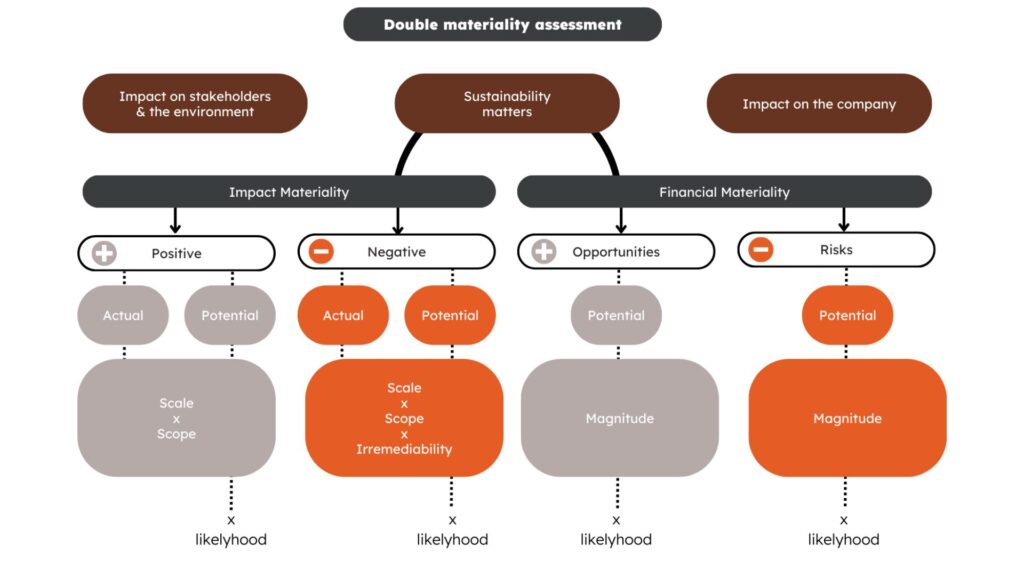

These key concepts form the foundation of the Double Materiality Assessment, explaining the dual focus on outward impacts on society and inward impacts on financial performance.

Double Materiality:

Graph 6: What is Double Materiality

This section contextualizes the Double Materiality Assessment within existing frameworks and standards, showcasing its evolution and the role of established guidelines.

The Double Materiality Assessment is a core component of the Corporate Sustainability Reporting Directive (CSRD), set to significantly change corporate sustainability reporting. This guide aims to help companies understand and implement this comprehensive reporting framework, which will impact around 50,000 companies. The CSRD mandates that companies report on how various sustainability issues affect ESG topics and vice versa, reflecting a comprehensive view of their environmental and social responsibilities.

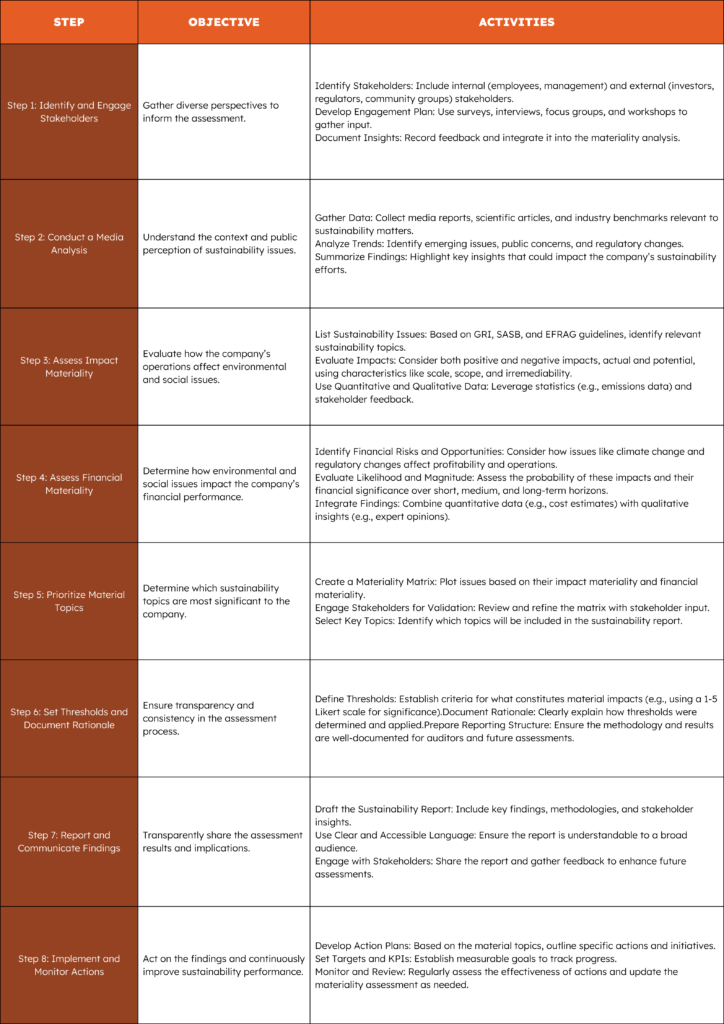

Double Materiality Step-by-Step Guide

By following this comprehensive step-by-step guide, companies can effectively conduct a Double Materiality Assessment, ensuring they meet regulatory requirements and enhance their sustainability practices. Engaging stakeholders, using robust methodologies, and maintaining transparency throughout the process will contribute to a more resilient and responsible business strategy. For more detailed guidance and tools, companies can refer to resources provided by GRI, SASB, EFRAG, and CSRD.

Understanding these characteristics helps companies effectively assess the significance of various impacts and their implications.

Graph 7: Double materiality Illustration

Implementing these assessments involves using both quantitative data and qualitative insights to evaluate materiality comprehensively.

This process requires a thoughtful methodology, including stakeholder engagement to identify and evaluate material impacts, risks and opportunities. It ultimately determines the ESRS that are applicable to the company and informs substantial parts of the company’s reporting.

Graph 8: Materiality assessment of sustainability data

This dual approach of the double materiality assessment ensures a thorough evaluation of both how a company affects the environment and society and how environmental and social factors, in turn, could impact the company.

Not All ESRS Need to be Included

Clarifying that not all ESRS topics need to be included ensures companies focus on the most relevant and significant issues.

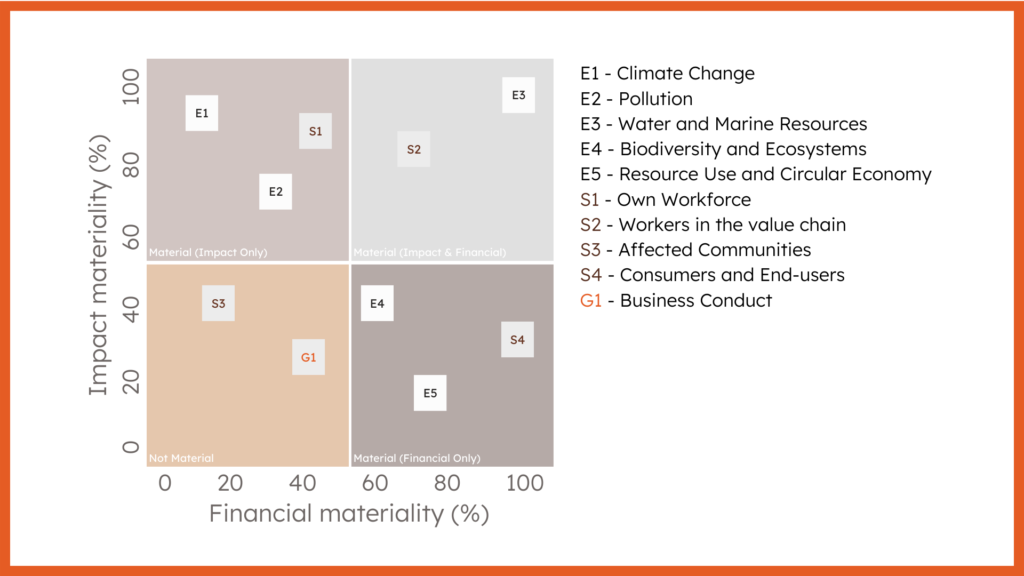

Companies are required to assess each of the 10 ESRS topics but are not obligated to include all in their sustainability reports. The Double Materiality Assessment helps determine which ESRS topics are material to the company’s operations and strategy. These topics are broken down into sub-topics and sub-sub-topics to ensure a thorough evaluation. For example:

This detailed assessment ensures that only the most relevant and significant topics are included in the company’s annual sustainability report, aligning with both the company’s strategic goals and regulatory requirements.

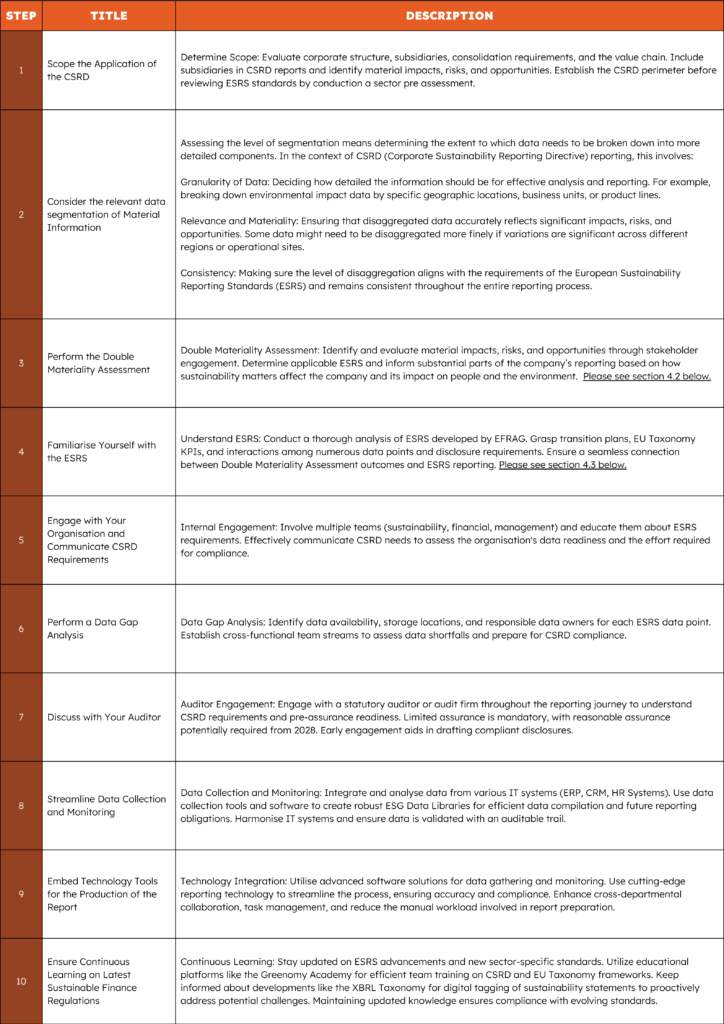

To ensure a seamless integration between the results of the Double Materiality Assessment and reporting under the European Sustainability Reporting Standards (ESRS), companies should thoroughly analyse the ESRS developed by EFRAG. Determining the applicable CSRD requirements involves following a specific methodology and necessitates a comprehensive understanding of the guidelines.

The CSRD introduces new sustainability aspects that may be complex for organizations to fully comprehend, such as the inclusion of transition plans and the key performance indicators (KPIs) outlined in the EU Taxonomy.

Moreover, ESRS reports require handling a substantial amount of data, with up to 1,200 data points and over 80 disclosure requirements that can interact with one another. Understanding these interactions is crucial for the successful execution of reporting obligations.

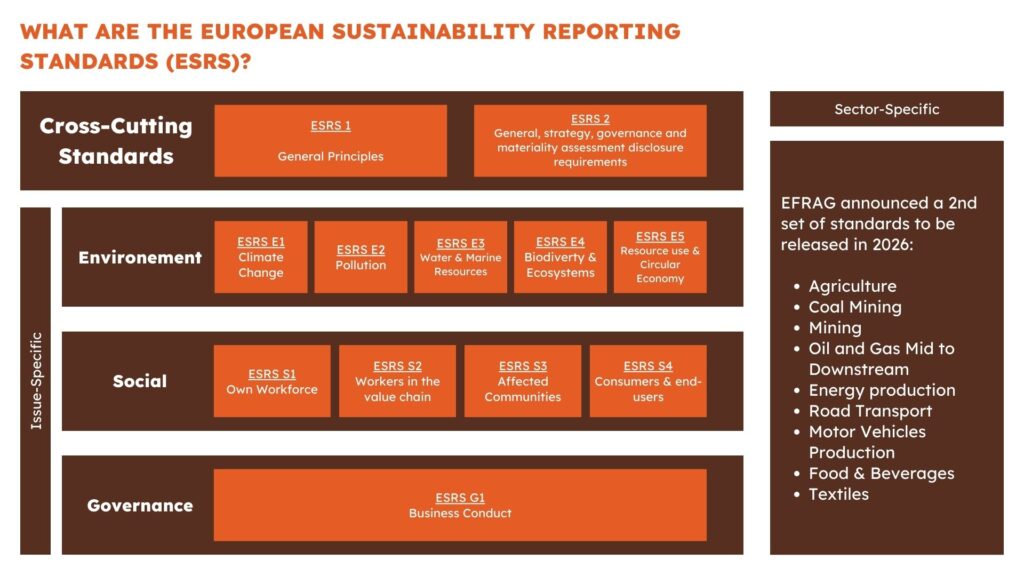

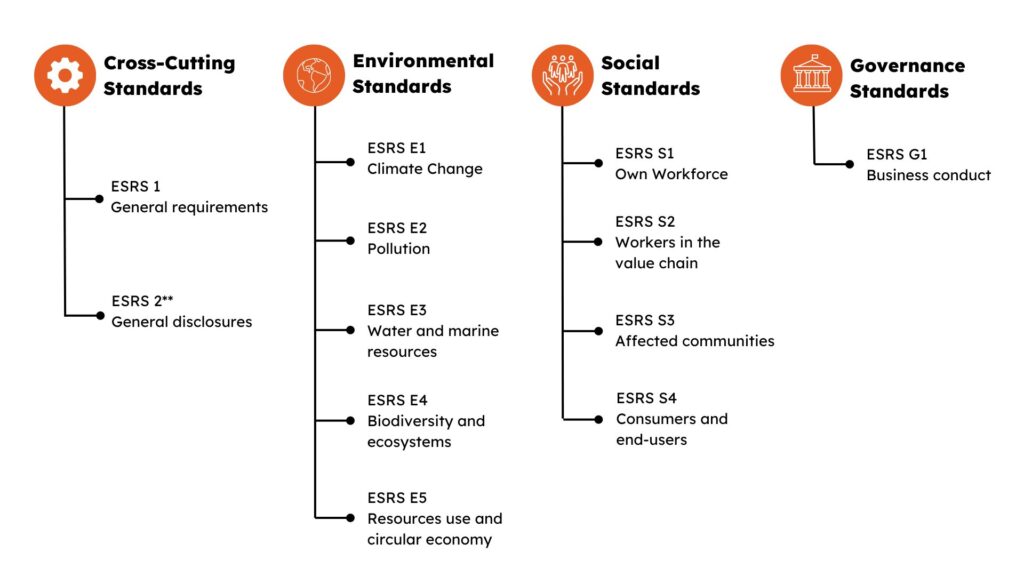

The ESRS are the detailed reporting standards that companies must adhere to in order to comply with the Corporate Sustainability Reporting Directive (CSRD). They provide a standardized framework for disclosing environmental, social, and governance (ESG) information, promoting transparency and comparability across the EU.

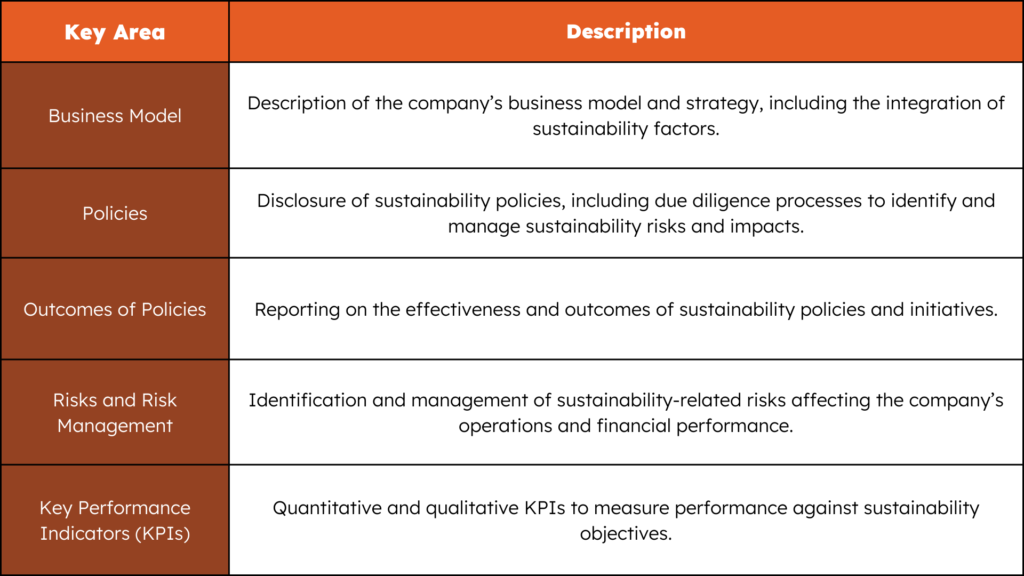

The CSRD mandates the disclosure of information across five key areas:

The ESRS are organized into different sets tailored for specific types of companies:

The full ESRS set comprises three categories:

Key Points to Note:

By understanding the structure and requirements of the ESRS, companies can prepare for compliance with the CSRD and effectively communicate their sustainability performance to stakeholders.

Graph 9: High level CSRD reporting standards

**Regardless of the double materiality assessment results, CSRD requires disclosure against these topics.

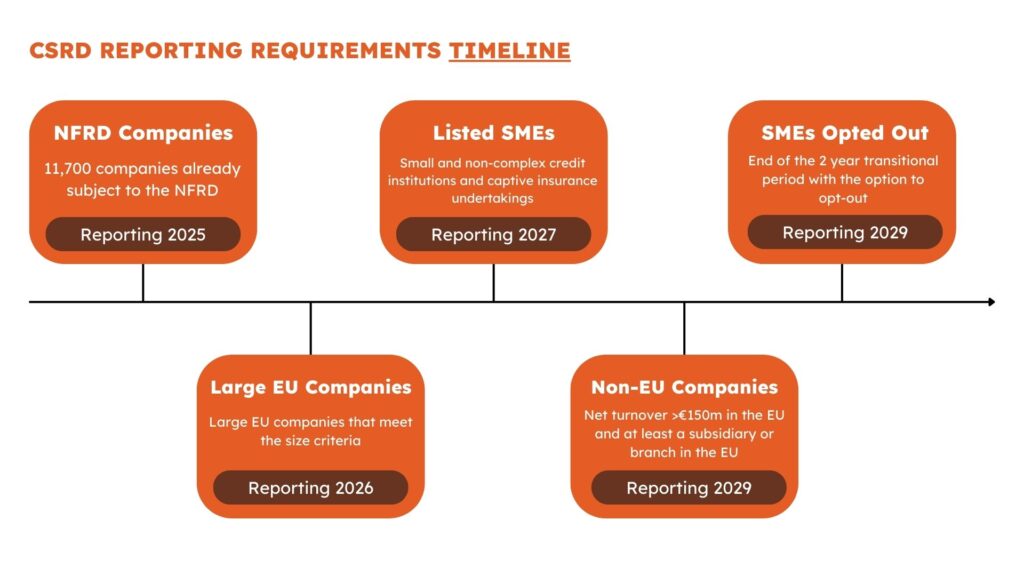

The CSRD will be phased in over several years. Larger companies already covered by the NFRD will start reporting from the fiscal year 2024. SMEs will begin reporting from 2026, and non-EU companies with significant EU operations will follow from 2028.

Graph 10: When do in scope companies need to report?

Informal terminology :

While the CSRD implementation is phased in, the official documentation and guidelines do not refer to these phases as “Tranche 1,” “Tranche 2,” and “Tranche 3.” Instead, they typically refer to them by the year they come into effect or the specific types of companies included in each phase.

However, for ease of reference, some stakeholders might informally refer to them as tranches. In that case, the breakdown would be:

Remember that this is not official terminology but rather a way some might simplify the different phases of implementation.

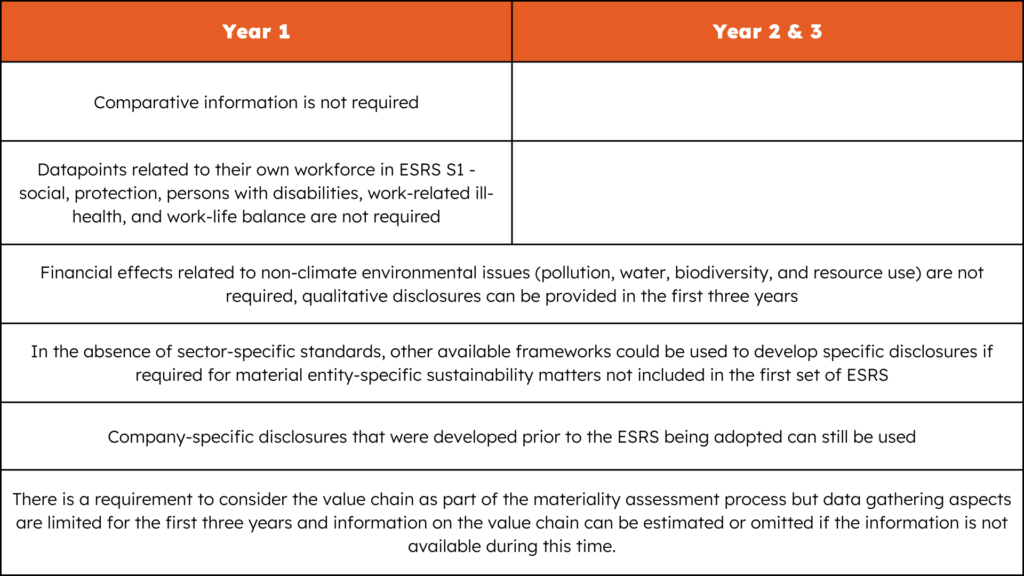

In the first year of reporting under the Corporate Sustainability Reporting Directive (CSRD), certain exemptions and transitional provisions are available to facilitate a smoother transition for companies. Here are the key exemptions:

Graph 11: Data exemptions CSRD in early years